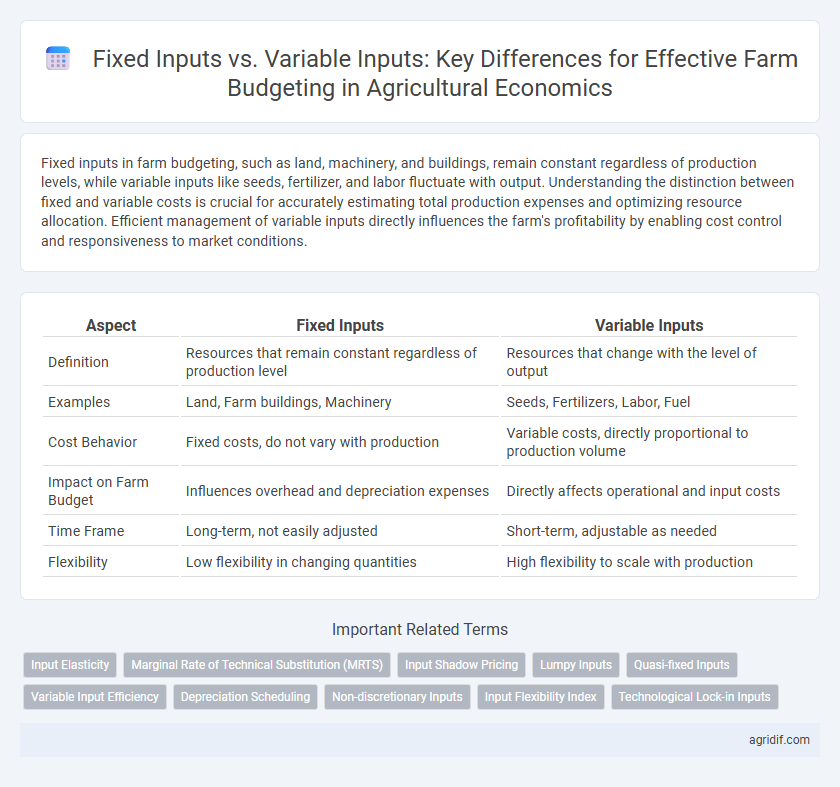

Fixed inputs in farm budgeting, such as land, machinery, and buildings, remain constant regardless of production levels, while variable inputs like seeds, fertilizer, and labor fluctuate with output. Understanding the distinction between fixed and variable costs is crucial for accurately estimating total production expenses and optimizing resource allocation. Efficient management of variable inputs directly influences the farm's profitability by enabling cost control and responsiveness to market conditions.

Table of Comparison

| Aspect | Fixed Inputs | Variable Inputs |

|---|---|---|

| Definition | Resources that remain constant regardless of production level | Resources that change with the level of output |

| Examples | Land, Farm buildings, Machinery | Seeds, Fertilizers, Labor, Fuel |

| Cost Behavior | Fixed costs, do not vary with production | Variable costs, directly proportional to production volume |

| Impact on Farm Budget | Influences overhead and depreciation expenses | Directly affects operational and input costs |

| Time Frame | Long-term, not easily adjusted | Short-term, adjustable as needed |

| Flexibility | Low flexibility in changing quantities | High flexibility to scale with production |

Defining Fixed Inputs in Agricultural Production

Fixed inputs in agricultural production refer to resources such as land, machinery, and buildings that remain constant regardless of the level of output. These inputs incur consistent costs during a budgeting period and do not vary with short-term changes in production volume. Understanding fixed inputs is essential for accurately estimating farm overhead and managing long-term investment decisions.

Understanding Variable Inputs on the Farm

Variable inputs in farm budgeting include seeds, fertilizers, labor, and fuel, whose quantities and costs fluctuate with the level of production. Efficient management of variable inputs directly influences crop yield, cost-efficiency, and overall farm profitability. Understanding the impact of variable input decisions is crucial for optimizing resource allocation and achieving sustainable agricultural production.

Key Differences Between Fixed and Variable Inputs

Fixed inputs in agricultural economics refer to resources such as land, machinery, and buildings that remain constant regardless of the level of production, while variable inputs like seeds, fertilizers, and labor change directly with output volume. Fixed inputs incur costs that do not fluctuate in the short term, impacting farm budgeting through fixed costs, whereas variable inputs affect variable costs and provide flexibility for adjusting production levels. Understanding these distinctions is crucial for optimizing cost management, improving profit margins, and making informed decisions in farm budgeting and resource allocation.

Impact of Fixed Inputs on Farm Budgeting

Fixed inputs such as land, machinery, and buildings represent capital investments that remain constant regardless of production levels, significantly influencing the structure of farm budgets by imposing unavoidable costs. These fixed costs necessitate careful allocation and long-term planning to optimize resource use and ensure economic viability. Understanding the impact of fixed inputs is crucial for accurate cost forecasting, risk assessment, and optimizing overall farm profitability.

Role of Variable Inputs in Cost Management

Variable inputs such as seeds, fertilizers, and labor directly influence the production level and allow farmers to adjust costs based on crop requirements and market conditions. Effective management of variable inputs reduces marginal costs and enhances overall farm profitability by aligning input usage with output goals. Tracking variable input expenses provides critical data for optimizing budget allocations and improving cost efficiency in agricultural operations.

Fixed Inputs: Examples and Budget Implications

Fixed inputs in farm budgeting include assets like land, machinery, and buildings, which remain constant regardless of production levels. These inputs incur fixed costs, such as depreciation, property taxes, and insurance, which must be accounted for even when output is zero. Understanding fixed inputs is crucial for accurate cost allocation and long-term financial planning within agricultural enterprises.

Variable Inputs: Types and Financial Planning

Variable inputs in farm budgeting include seeds, fertilizers, pesticides, labor, and fuel, which fluctuate based on production levels and directly affect short-term costs. Accurate estimation of these variable costs is crucial for financial planning to optimize resource allocation and maximize profit margins. Monitoring market prices and usage rates of variable inputs helps farmers develop adaptive budgeting strategies that improve cost efficiency and crop yield outcomes.

Balancing Fixed and Variable Inputs for Optimal Profitability

Balancing fixed inputs such as machinery, land, and infrastructure with variable inputs like seeds, fertilizers, and labor is crucial for maximizing farm profitability. Efficient allocation ensures fixed costs are spread over sufficient production levels while variable inputs adjust to market conditions, optimizing marginal returns. Precision in managing this balance drives cost-efficiency and sustainable revenue growth in agricultural economics.

Strategies to Manage Input Costs in Agriculture

Managing input costs in agriculture requires distinguishing between fixed inputs, such as land and equipment, and variable inputs like seeds, fertilizers, and labor, which fluctuate with production levels. Implementing precision agriculture techniques and adopting cost-effective supply chain practices can optimize variable input usage, enhancing overall budget efficiency. Strategic contract arrangements and investment in durable fixed assets enable long-term cost control and improved financial planning within farm budgeting.

Fixed vs Variable Inputs: Decision-Making in Farm Resource Allocation

Fixed inputs in farm budgeting, such as land, machinery, and permanent structures, remain constant regardless of production levels and significantly impact long-term capital allocation. Variable inputs, including seeds, fertilizers, and labor, fluctuate with crop production intensity, directly influencing short-term operational costs and yield outcomes. Effective decision-making in farm resource allocation requires balancing fixed and variable inputs to optimize cost efficiency and maximize profitability under changing market conditions.

Related Important Terms

Input Elasticity

Fixed inputs in farm budgeting, such as land and machinery, exhibit low input elasticity since their quantities remain constant regardless of output changes, while variable inputs like labor and fertilizers have higher input elasticity, allowing adjustments in response to production needs. Understanding the differing elasticities of fixed and variable inputs enables more accurate cost management and optimization of resource allocation in agricultural production.

Marginal Rate of Technical Substitution (MRTS)

Fixed inputs, such as land and machinery, remain constant in farm budgeting regardless of production levels, while variable inputs like labor and fertilizers adjust to optimize output. The Marginal Rate of Technical Substitution (MRTS) measures the rate at which a farmer can substitute one variable input for another while maintaining the same level of production, crucial for cost-effective resource allocation in agricultural economics.

Input Shadow Pricing

Fixed inputs in farm budgeting, such as land and machinery, have shadow prices reflecting their opportunity costs in scenarios where quantities are constrained, while variable inputs like labor and fertilizer exhibit shadow prices that capture the marginal cost of adjusting input levels. Accurate shadow pricing of both fixed and variable inputs is essential for optimizing resource allocation, maximizing farm profitability, and guiding efficient decision-making under budget constraints in agricultural economics.

Lumpy Inputs

Lumpy inputs in farm budgeting refer to fixed inputs that cannot be easily adjusted in the short run, such as tractors or irrigation systems, which require significant investment and are used over multiple production cycles. Understanding the impact of these lumpy inputs helps optimize resource allocation by distinguishing them from variable inputs like seeds and labor, which can be adjusted more frequently in response to changing production needs.

Quasi-fixed Inputs

Quasi-fixed inputs in farm budgeting refer to inputs that exhibit fixed costs within certain capacity ranges but can be adjusted or varied over longer time horizons, such as machinery or irrigation systems. These inputs bridge the gap between fixed and variable inputs by allowing some flexibility in resource allocation while maintaining relative cost stability in the short term, impacting farm cost structures and production planning.

Variable Input Efficiency

Variable input efficiency in farm budgeting measures how effectively resources like seeds, fertilizers, and labor are utilized to maximize crop yield per unit cost. Optimizing variable inputs enhances profitability by reducing waste and improving marginal returns without altering fixed assets such as land and machinery.

Depreciation Scheduling

Fixed inputs in farm budgeting, such as machinery and buildings, incur depreciation that must be scheduled systematically to allocate costs evenly over their useful lives, ensuring accurate long-term financial planning. Variable inputs like seeds and labor fluctuate with production levels and do not involve depreciation, highlighting the importance of differentiating these inputs for precise cost management and profitability analysis.

Non-discretionary Inputs

Non-discretionary inputs in farm budgeting refer to fixed inputs such as land, machinery, and permanent labor, which remain constant regardless of the level of production. These inputs create baseline costs that farmers must cover before considering variable inputs like seeds or fertilizers, impacting overall financial planning and economic efficiency.

Input Flexibility Index

Fixed inputs, such as land and machinery, remain constant regardless of production volume, while variable inputs like seeds and fertilizers change with output levels; the Input Flexibility Index measures the ease with which a farm can adjust input quantities in response to changing economic conditions. A higher Input Flexibility Index indicates greater adaptability in reallocating resources to optimize cost-efficiency and maximize profitability in farm budgeting.

Technological Lock-in Inputs

Technological lock-in inputs in farm budgeting refer to fixed inputs that limit a farm's ability to adapt to new technologies, often including specialized machinery or infrastructure tailored to specific crops or methods. These fixed inputs create economic rigidity by increasing sunk costs, making variable inputs like labor and fertilizer adjustments less effective in improving overall productivity or cost-efficiency.

Fixed inputs vs Variable inputs for farm budgeting Infographic