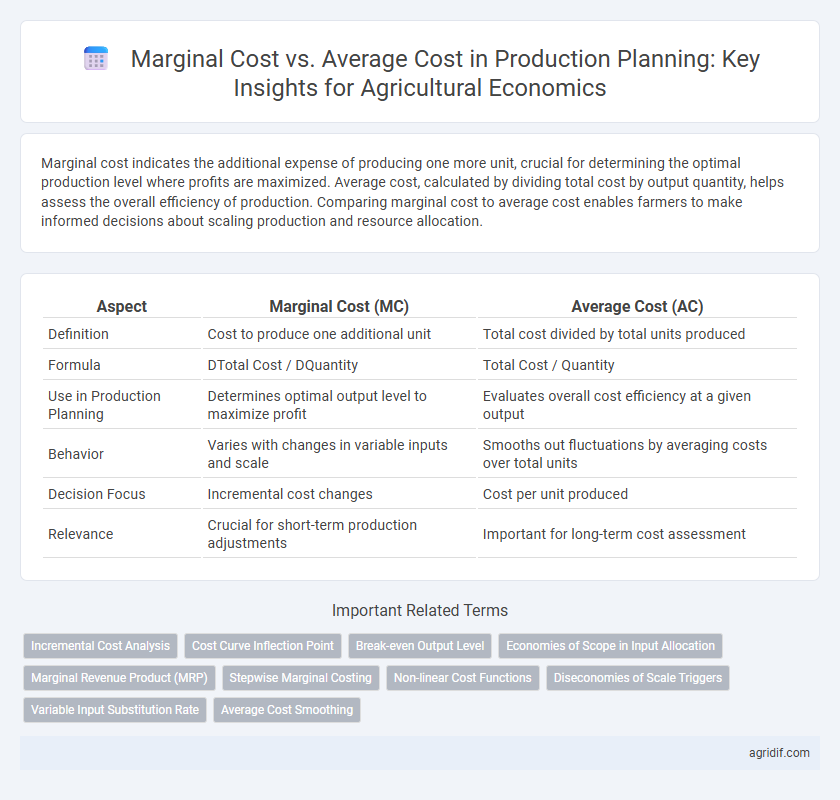

Marginal cost indicates the additional expense of producing one more unit, crucial for determining the optimal production level where profits are maximized. Average cost, calculated by dividing total cost by output quantity, helps assess the overall efficiency of production. Comparing marginal cost to average cost enables farmers to make informed decisions about scaling production and resource allocation.

Table of Comparison

| Aspect | Marginal Cost (MC) | Average Cost (AC) |

|---|---|---|

| Definition | Cost to produce one additional unit | Total cost divided by total units produced |

| Formula | DTotal Cost / DQuantity | Total Cost / Quantity |

| Use in Production Planning | Determines optimal output level to maximize profit | Evaluates overall cost efficiency at a given output |

| Behavior | Varies with changes in variable inputs and scale | Smooths out fluctuations by averaging costs over total units |

| Decision Focus | Incremental cost changes | Cost per unit produced |

| Relevance | Crucial for short-term production adjustments | Important for long-term cost assessment |

Understanding Marginal Cost in Agricultural Production

Marginal cost in agricultural production represents the additional expense incurred by producing one more unit of output, crucial for optimizing resource allocation and maximizing profitability. It directly influences production decisions by comparing the cost of increasing output against potential revenue, unlike average cost which spreads total costs over all units produced. Understanding marginal cost helps farmers and agribusinesses determine the most efficient scale of operation and adjust input usage precisely to respond to market conditions and minimize waste.

Defining Average Cost in Farm Operations

Average cost in farm operations represents the total cost of production divided by the quantity of output produced, providing a per-unit cost metric essential for economic decision-making. It encompasses fixed costs, such as land rent and equipment depreciation, and variable costs, including seeds, labor, and fertilizers. Understanding average cost aids farmers in identifying efficient production levels, optimizing resource allocation, and evaluating profitability against market prices.

Key Differences Between Marginal and Average Costs

Marginal cost measures the additional expense incurred by producing one more unit of output, while average cost represents the total cost divided by the quantity produced. Marginal cost influences short-term production decisions, as it helps identify the optimal output level to maximize profit. Average cost reflects overall efficiency and economies of scale, guiding long-term planning and pricing strategies in agricultural production.

Calculating Marginal Cost for Crop Yields

Calculating marginal cost for crop yields involves determining the additional cost incurred by producing one more unit of output, which helps optimize resource allocation in agricultural production. Marginal cost is derived from changes in total cost divided by changes in output, emphasizing variable inputs like seeds, fertilizers, and labor per incremental yield increase. Comparing marginal cost to average cost guides producers in identifying the most efficient production level to maximize profitability and sustainable crop management.

Assessing Average Cost in Livestock Enterprises

Assessing average cost in livestock enterprises involves calculating the total production costs divided by the number of units produced, providing a baseline for evaluating cost efficiency. Marginal cost represents the additional cost incurred by producing one more unit, which is critical for making decisions on scaling production. Comparing marginal cost to average cost helps identify the optimal production level where economies of scale are maximized and profitability is enhanced.

Implications of Cost Structures on Production Planning

Marginal cost, reflecting the cost of producing one additional unit, is crucial for determining optimal output levels in agricultural production, as it directly influences decisions on scaling operations. Average cost provides insight into overall efficiency by dividing total cost by output, helping identify economies of scale and cost-saving opportunities in resource allocation. Understanding the relationship between marginal and average cost helps farmers and agribusinesses plan production to minimize costs and maximize profitability under varying market conditions.

Marginal Cost and Decision-Making in Agriculture

Marginal cost represents the cost of producing one additional unit of output, playing a crucial role in agricultural production planning by guiding resource allocation decisions to maximize profitability. When marginal cost falls below average cost, expanding production can reduce overall costs, while marginal cost above average cost signals a need to scale back to avoid losses. Farmers rely on marginal cost analysis to optimize input use, such as labor and fertilizers, ensuring efficient production that aligns with market prices and demand fluctuations.

Average Cost Analysis for Profit Maximization

Average cost analysis is crucial for profit maximization in agricultural production planning as it helps identify the cost per unit of output by dividing total cost by the quantity produced. Understanding how average cost behaves at different production levels enables farmers to determine the optimal scale of operation where profits are maximized. Monitoring average cost alongside marginal cost ensures efficient resource allocation and prevents overproduction that can erode profit margins.

Integrating Cost Concepts into Farm Management Strategies

Marginal cost represents the additional expense incurred from producing one more unit of output, while average cost reflects the total cost divided by the quantity produced. Understanding the relationship between marginal and average cost is critical for optimizing resource allocation and maximizing farm profitability in production planning. Integrating these cost concepts into farm management strategies enables precise decision-making regarding production levels, input use, and cost control to enhance overall economic efficiency.

Optimizing Resource Allocation: Marginal vs Average Cost

Marginal cost reflects the expense of producing one additional unit, crucial for determining the optimal level of input use in agricultural production, while average cost measures the total cost per unit over all output levels. Efficient resource allocation occurs when marginal cost equals marginal revenue, guiding farmers to adjust production to maximize profits and minimize waste. Comparing marginal and average costs helps identify the point where expanding production is cost-effective versus when it leads to diminishing returns, optimizing farm resource investments.

Related Important Terms

Incremental Cost Analysis

Marginal cost represents the additional expense incurred by producing one more unit, while average cost reflects the total cost divided by output, both critical for incremental cost analysis in agricultural production planning. Evaluating marginal cost against average cost helps optimize resource allocation, ensuring efficient scale and minimizing waste in crop or livestock production.

Cost Curve Inflection Point

The inflection point on the cost curve marks the transition where marginal cost surpasses average cost, indicating increased inefficiency in resource allocation during production. Understanding this threshold is crucial in agricultural economics, as it guides producers in optimizing input use to minimize costs and maximize profit margins.

Break-even Output Level

Marginal cost (MC) intersects average cost (AC) at the break-even output level, signaling the point where producing additional units begins to decrease average cost and firms start covering total costs. Understanding this relationship is crucial in agricultural production planning to optimize resource allocation and achieve cost-efficiency in crop or livestock management.

Economies of Scope in Input Allocation

Marginal cost measures the expense of producing one additional unit, while average cost reflects total production expense divided by output quantity, both crucial for optimizing input allocation in production planning. Economies of scope arise when shared inputs reduce overall costs across multiple products, enhancing efficiency by lowering combined marginal and average costs in diversified agricultural systems.

Marginal Revenue Product (MRP)

Marginal cost (MC) represents the additional expense incurred from producing one more unit of output, while average cost (AC) measures the total cost per unit produced. In production planning, optimizing input use involves equating Marginal Cost to the Marginal Revenue Product (MRP), ensuring resources are allocated where the value of the additional output equals its cost.

Stepwise Marginal Costing

Stepwise marginal costing analyzes production costs by evaluating incremental cost increases associated with additional output levels, offering precise insight for resource allocation decisions. This method contrasts with average cost analysis, which smooths cost data, potentially obscuring the specific impact of variable inputs on production planning efficiency.

Non-linear Cost Functions

In agricultural economics, understanding the distinction between marginal cost and average cost is crucial for production planning, especially when dealing with non-linear cost functions where costs do not increase proportionally with output. Marginal cost represents the cost of producing one additional unit, often varying due to factors like diminishing returns or input constraints, while average cost reflects total cost divided by output, both influencing optimal input allocation and profitability decisions.

Diseconomies of Scale Triggers

Marginal cost tends to rise above average cost when diseconomies of scale occur due to factors like increased input prices, management inefficiencies, and resource overuse that reduce production efficiency. Identifying these triggers in agricultural production planning helps optimize input allocation and prevent cost escalations that lower overall farm profitability.

Variable Input Substitution Rate

Marginal cost reflects the additional expense of producing one more unit of output, directly influenced by the variable input substitution rate as farmers adjust inputs like labor and fertilizer to optimize efficiency. Understanding the interplay between marginal cost and average cost enables more precise production planning, as shifts in the substitution rate impact input allocation and overall cost structures in agricultural operations.

Average Cost Smoothing

Marginal cost significantly influences production decisions by indicating the expense of producing one additional unit, while average cost smoothing helps stabilize cost fluctuations over varying output levels, facilitating more reliable budgeting and long-term planning. Employing average cost smoothing reduces the impact of short-term cost volatility, enabling farmers and agribusiness managers to allocate resources efficiently and optimize profitability in agricultural operations.

Marginal cost vs average cost for production planning Infographic